The Rupredicament — A Steadier Hand for Delhi

What India should — and should not — do as the Rupee tests new lows, reserves bleed, and the 2013 reflex returns. Five steps, in order. And three to avoid.

TL;DR

The rupee at 95.31 is a shock with two distinct legs — a terms-of-trade hit from Brent above $104 and a capital account hit from $21 billion of YTD foreign portfolio outflows. The legs need different instruments. The instinct to hike rates against the latter is the 2013 mistake.

The sequence, in order: (1) stand up an oil-importer swap window of the 2013 design to take OMC dollar demand out of the spot market; (2) raise dollar inflows through a redesigned scheme that prices the hedge via auction and opens beyond NRI deposits to banks, quasi-sovereigns, and ECB issuers; (3) ease the FPI inflow side — residual maturity, corporate bond limits, FAR menu; (4) substitute, do not prohibit, on gold demand via Sovereign Gold Bonds; (5) hold the rate decision in reserve. The June MPC should hold.

What not to do: lower the LRS limit, announce a defended rupee band, or make the PM’s Sunday speech a recurring address. Each carries signaling damage far beyond the BOP arithmetic.

Why this matters: India in 2026 has the deepest reserves, strongest banking system, most credible inflation framework, and lowest current account deficit in its history of dealing with crises of this kind. The 1991 and 2013 playbooks are not the right reference. Use the instruments built for this moment, sequence them, communicate the plan — and beyond cyclical defense, work to close the structural gap in the external account.

The Prime Minister’s Sunday address asked Indians to conserve fuel, postpone foreign holidays, and pause gold purchases. Within twenty-four hours the rupee printed a fresh record low intraday at 95.31. The Sensex shed 1,313 points. Jewelry stocks were down eleven percent. The market did not read the speech as resolve. It read it as alarm.

That is the first thing Delhi must fix. The shock India is absorbing is real. But the policy menu has more instruments today than the 2013 playbook everyone keeps reaching for. The question is sequencing.

The shock has two legs. The response should too.

Leg one is a terms-of-trade shock: Brent above $104, India importing ninety percent of its crude, the import bill widening in real time. Leg two is a capital account shock: roughly $21 billion of foreign portfolio outflows year-to-date, the dollar firm on US data, EM under pressure. Different problems. Different instruments. Conflating them — reaching for the rate-hike hammer — is the 2013 mistake.

What the tape is telling us

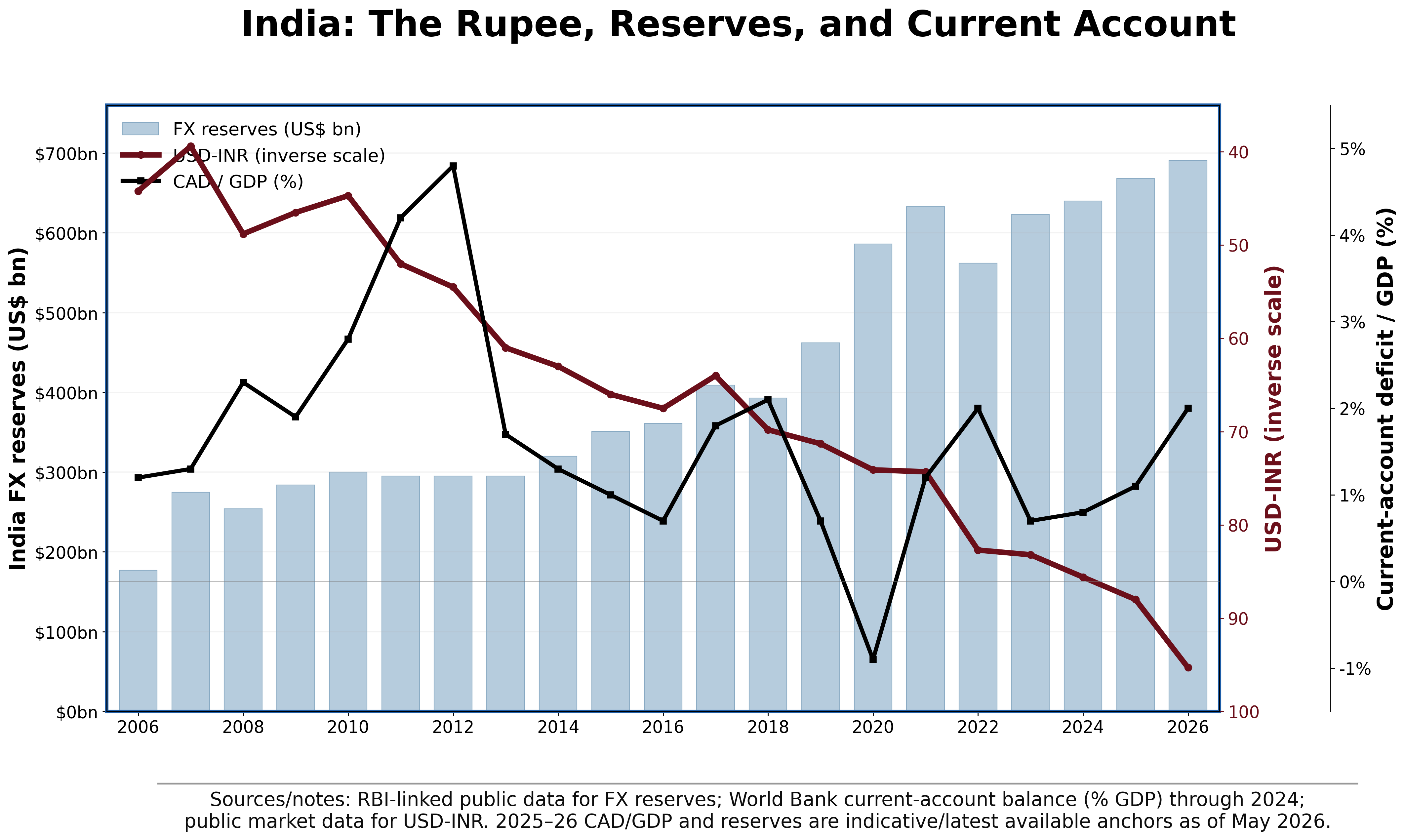

The RBI has done the right thing first. Sell dollars into disorderly moves. Lean against the one-way crowd in NDF. Tighten the arbitrage between onshore and offshore. Reserves at $690.7 billion as of May 1, down from the $728.5 billion peak in late February, buy time but not patience. At the current intervention pace, the headline number will be inside $650 billion within a quarter. That is still eleven months of import cover. It is also a falling line on every emerging-market screen in London and Singapore.

Interest rate swaps now price seventy basis points of RBI hikes over twelve months. That is the market’s pricing a panic response that has not happened. The MPC should not validate it.

The ten-year G-Sec is trading near seven percent against a March headline CPI of 3.4 percent. The real yield is the highest it has been in over a decade. India does not have an inflation problem. It has a pass-through risk on the import bill and a confidence problem in the currency. Different instruments.

Hike rates here and you solve neither. You compound the supply shock with a demand contraction and tell every foreign allocator that India panicked first.

The sequence

Do these in order. Do not do them all at once. And communicate each step as a coherent plan rather than a list of measures.

First, defend the terms of trade directly. Stand up an oil-importer swap window now, before reserves bleed another twenty billion across the spot tape. The mechanism RBI deployed in August 2013 — OMCs swap rupees for dollars with the central bank under a forward agreement to reverse — takes the largest single source of daily dollar demand out of the spot market without spending reserves at fire-sale prices. It is the highest-leverage move available. It should be the first announcement.

Second, lengthen the dollar inflow pipe. The 2013 FCNR-B window raised $26 billion in three months. It worked, but for reasons worth understanding before reaching for it again (see the section that follows). The redesigned instrument should price the hedge through a transparent auction of RBI forwards rather than a fixed subsidy, and open the window beyond NRI deposits to all approved foreign currency borrowers. Let banks and quasi-sovereigns bid for the swap on equal terms. The cost is contained. The inflow is honest. The signal is that India is opening the door wider, not building higher walls.

Third, ease the capital account on the inflow side, not just the outflow side. Cut the FPI minimum residual maturity on government bonds. Raise the aggregate FPI limit on the corporate bond market. Reopen the fully-accessible-route bond menu to longer tenors. The JPM index inclusion is doing the slow work of structural inflows; accelerate it with administrative moves that cost nothing and signal openness. Standard Chartered’s note this morning gets this right. Delhi can move on it this week.

Fourth, and only fourth, look at demand-side measures on imports. Raising the gold customs duty is a tempting headline. It is also a smuggling subsidy and a regressive tax on Indian household wealth that simply migrates the flow offshore. The 2022 increase taught us that. If gold demand must be addressed, do it on the price elasticity: extend the Sovereign Gold Bond program with a more attractive coupon, restart issuance, and divert the next festival-season flow from physical bullion into a paper instrument that does not consume reserves. Substitution, not prohibition. Prohibition has never worked in Indian gold markets and will not start now.

Fifth, hold the rate decision in reserve. The June MPC should hold. If oil sustains above $110 for a quarter and second-round effects appear in core CPI, then a measured twenty-five basis-point move is defensible. Until then, the rate path is the wrong place to fight a current-account war. The market is asking for a hike. The market is wrong.

Lessons learnt from 2013

Three things worked then. Three things did not. Worth separating them before reaching for the playbook.

The headline numbers from 2013 are well known. The two swap windows brought in $34 billion at a critical moment — $26 billion through the three-year FCNR-B route and $8 billion through the parallel bank ECB swap. The rupee stabilized. Confidence returned. The oil swap window worked. It shifted the largest single source of daily dollar demand to a forward date and gave the spot market room to breathe. The communication discipline of the new RBI Governor worked. Raghuram Rajan’s first press conference did more for the currency than the next month of intervention.

The less-told story is what the $26 billion actually was. The headline framed it as patriotic NRI deposits coming home in the country’s hour of need. NRIs at the time received term sheets from banks structuring the trade. The concessional swap was the entire reason the trade existed. Strip it out and the flow does not happen. The diaspora narrative was the wrapper. The substance was bank-intermediated carry.

This matters now because the same instrument is being eyed again. The structural flaw of the 2013 design was the form, not the headline number. RBI wrote a subsidized forward cover that took the FX risk onto its own books, and the concessional access was gated through a single retail channel. The redesigned instrument should price the hedge through a transparent auction and open the window to all approved foreign currency borrowers — banks, quasi-sovereigns, ECB issuers — on the same terms. The 2013 bank window itself cleared at a 1 percent subsidy against the NRI window’s 3 percent, both on RBI’s books. That differential is the cost of the diaspora wrapper. Remove the wrapper, give institutional capital its own door, and the same dollars come in at materially lower cost to the sovereign.

Two further pieces of the 2013 playbook should not be revived. The two-hundred-basis-point hike in the Marginal Standing Facility rate in July 2013 was reversed within four months because it strangled growth without solving the FX problem. And the gold import restrictions of August 2013 produced a domestic smuggling industry that took years to unwind.

The instruments to revive are clear. So is what to leave on the shelf — and what to redesign before the headline is recycled.

What not to do

Do not lower the LRS limit. The Liberalized Remittance Scheme cap at $250,000 is a freedom the Indian middle class has earned over two decades. Cutting it saves a rounding error in the balance of payments and tells every Indian saver that capital controls are back on the table. The signaling damage compounds for years. India is a capital-importing economy. The brand it has spent twenty-five years building is that capital flows freely in both directions. Do not vandalize that brand for a quarter’s optics.

Do not announce a target band for the rupee. Reserve management works precisely because there is no defended level. The moment 95 becomes the line in the sand, every macro fund on the planet sells dollars against the RBI and stops selling when they see the bid disappear. Intervene against volatility, not against a level. Continue what is already being done. Do not give it a name.

Do not make the Sunday speech a recurring address. Asking citizens to forego foreign travel and gold purchases is the wrong instrument and the wrong forum. It conflates a price-mechanism problem with a moral exhortation. It tells markets that the government is anxious. Modi’s political capital is too valuable to spend on a currency line. The institutional voice for FX is the RBI Governor. The voice for fiscal headroom is the Finance Minister. The PM’s office should hold the macro framing, not the micro behavior.

The framing Delhi needs

A piece of communication has been missing from the past week. The one that says: this is a supply shock common to every oil importer; India is better positioned than most because reserves are deep, the fiscal glide path is intact, the inflation framework was just reaffirmed at four percent for another five years, and the banking system is recapitalized. The plan is calibrated. The plan is sequenced. The plan does not require households to change behavior. That message, delivered by the right institutional voice, would do more for the rupee than another five billion of spot intervention.

The rupee will find its level. The question is what level. At what reputational cost and with how much of reserves consumed in the process. The instruments to manage this exist. The 1991 playbook is not the right playbook. Nor is 2013. India in 2026 is a fundamentally different economy — larger reserves, deeper bond market, stronger banking system, lower current account deficit, an inflation-targeting central bank with a decade of credibility behind it.

Use the instruments built for this moment. Sequence them. Communicate the plan. And keep the rate cudgel in the cupboard.

The market will read it as resolve. The diaspora may write the cheque again, but under the framework suggested here. And beyond cyclical defense, policy must work to close the structural gap in the external account.

References: Reuters, Reserve Bank of India, Standard Chartered Bank, Trading Economics, India Ministry of Statistics and Programme Implementation.

The Macro Fireside

Macrofireside.com · @Macrofireside on X

The Macro Fireside is a practitioner’s publication — written at the intersection of markets, policy, and geopolitics by an experienced hand who has spent decades managing money and financial markets risk through moments the world would only later recognize as inflection points. The author has also been a keen observer of the India macro story for long. Analysis here is earned, not assembled. This piece does not constitute investment advice.

For professional enquiries: gs@macrofireside.com