Fed Didn’t Move Its Dot Plot. The World Did.

A Practitioner’s Read on the March 2026 FOMC Statement, SEP, and What Comes Next

THE BOTTOM LINE

The Fed revised its 2026 inflation forecast up 30 basis points—and left the rate path unchanged. One member dissented in favor of a cut. The Committee explicitly named the Middle East conflict in its policy statement. The press conference added an edge the statement omitted: core PCE is tracking near 3%, private-sector job growth is near zero, and the tariff pass-through timeline is genuinely unknown.

Together, these facts constitute a quiet acknowledgment of the stagflation trap: inflation is worse than expected, growth is softening, and the cause of both is a war that monetary policy cannot fight. The market has since delivered a harder verdict: bond yields rising, dollar holding its bid, gold down over 3%. The initial dovish read on unchanged dots did not hold. Energy infrastructure and selective utilities are the cleaner expressions of this environment. Bonds and gold need the dollar to turn first.

The Statement: What Was Said—and What Wasn’t

At 2:00 PM today, the Federal Reserve did something worth sitting with. It told us, in the careful, desiccated language of central banking, that it expects inflation to run hotter than it previously thought—and that it is not going to do anything about it.

Two sentences in the statement stopped me cold.

“Job gains have remained low.”

That is a meaningful downgrade from prior language about a solid labor market. The employment side of the dual mandate is softening—quietly, but visibly.

“The implications of developments in the Middle East for the U.S. economy are uncertain.”

The Fed explicitly named the geopolitical event in its policy statement. This is rare. When the FOMC puts something in the statement, it is not an aside—it is a signal that the variable in question is now a primary driver of policy deliberation.

Taken together, the Fed is telling us: growth is softening, inflation is rising, and the cause of both is a war we cannot control. Welcome to the stagflation trap.

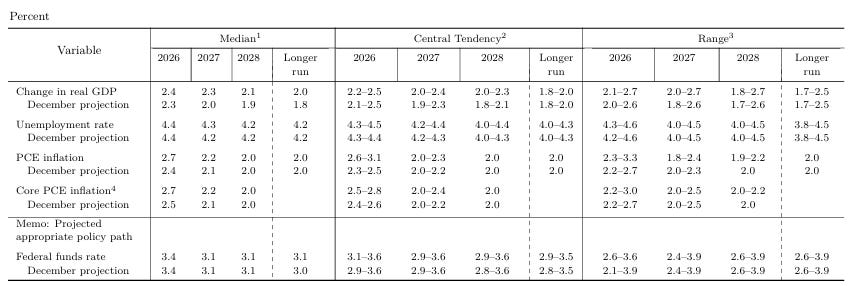

The SEP: The Numbers That Matter

The Summary of Economic Projections released alongside the statement contained the real story. Here is what changed from December to March:

GDP was revised up modestly. Inflation was revised up materially—thirty basis points on both headline and core PCE. And the projected federal funds rate for 2026? Unchanged at 3.4%.

The Fed upgraded its inflation forecast by 30 basis points and left the rate path untouched. This is not a neutral technical adjustment. This is a policy choice.

This is a policy choice—and a consequential one. The Fed is explicitly choosing to absorb the inflation revision rather than respond to it. In doing so, it is allowing real interest rates to drift lower even as nominal inflation expectations rise.

The Miran Dissent: The Most Telling Line

Buried in the vote tally is the most revealing data point of the entire release.

Governor Stephen Miran dissented—in favor of a 25 basis point cut.

One member of the Federal Open Market Committee looked at PPI running at 3.4% year-over-year, Brent crude above $109, Iranian forces attacking regional energy infrastructure, and South Pars—the world’s largest gas field—under strike, and concluded: we should be easing monetary policy today.

This is not a one-off outlier. Miran has dissented at every single FOMC meeting he has attended, each time in favor of larger rate cuts. Today’s vote is the continuation of a pattern, not an aberration. And that pattern tells you something important about where the Fed’s internal dovish flank sits—and how quickly it will move when the window reopens.

I am not here to argue that Miran is right. But the dissent record tells you the gravitational pull of the Fed’s cutting cycle—interrupted but not abandoned—is still very much alive.

When the geopolitical situation creates enough economic pain, or when growth data softens sufficiently, the path back to cuts will open faster than the dots currently suggest. The Miran dissent is your early warning indicator.

The Supply Shock Framework—and Its Limits

The Fed is clearly applying its established “supply shock” analytical framework to the current situation. The logic runs as follows: oil price spikes caused by geopolitical disruption are by definition transitory. They do not reflect underlying demand pressure. Therefore, a central bank that responds to supply-driven inflation by tightening policy risks imposing unnecessary economic pain on a slowing economy for a problem that will resolve itself when the disruption ends.

This framework is not unreasonable. It has historical precedent. And given that the Strait of Hormuz selective blockade — which is what we are actually dealing with, not a full closure—represents exactly the kind of supply-side disruption that tends to be time-limited, the Fed’s analytical instinct is defensible.

But there is a limit to this framework, and we may be approaching it.

South Pars has been struck. Saudi Arabia’s eastern province—the geographic heart of Aramco’s production infrastructure—has received incoming attack alerts. Insurance markets are repricing war risk across all Hormuz transits regardless of flag. Norway has withdrawn its flag-carrying vessels from the strait entirely.

If this situation persists for months rather than weeks, the supply shock framework begins to look less like analytical rigor and more like wishful thinking. The Fed has given itself the benefit of the doubt today. The question is whether events will extend that courtesy.

The Energy Dimension: Where the Fed Has No Answer

There is one element of today’s environment that the Fed’s framework simply cannot accommodate, and it is the most important one.

The selective Hormuz blockade is not a standard supply shock. It is a geopolitical weapon being deployed with strategic precision. Iran has not closed the strait—it has nationalized it. Western-linked vessels are barred or targeted; ships from “friendly” nations pass through under Iranian supervision. This is not a disruption that resolves when storm season ends or when a pipeline is repaired. It resolves when one of the parties to the conflict decides its negotiating objectives have been met.

The Fed cannot cut rates to fix a blockade. It cannot raise rates to end a war. It is, by the nature of the situation, a spectator to the most important variable in the economic outlook.

That helplessness—acknowledged implicitly in the phrase ‘implications of developments in the Middle East are uncertain’—is the subtext of today’s statement.

Powell at the Podium: Patience With an Edge

The press conference added texture—and a degree of hawkish undertone—that the statement alone did not fully convey.

Powell’s opening message was consistent with the statement: the economy is still expanding, consumer spending remains resilient, and the policy stance is appropriate. But the press conference revealed a Chair who is more uncomfortable about the inflation picture than the unchanged rate path might suggest.

On Inflation: Cautious, At Times Hawkish

Powell indicated that February PCE is tracking around 2.8%, with core PCE near 3%. He acknowledged that progress has been slower than hoped—particularly in non-housing services—and was unambiguous on the conditional: if inflation does not improve, there will be no rate cut.

He repeated the tariff framework—that pass-through should in theory be a one-time effect—but was careful to add that he is not at all certain that is how it will play out, and admitted the Fed does not know how long the pass-through will take. That is the Fed telling you its own inflation model carries wide error bars in the current environment.

On energy: some of the oil shock will show up in inflation, and while the Fed may eventually look through it, that becomes much harder after five years of inflation running above target.

That last clause is the most important sentence Powell delivered. Five years of above-target inflation has eroded the Fed’s ability to credibly invoke the “transitory” framework. The supply shock playbook is still available—but the political and institutional cost of using it has risen materially.

On Stagflation: Pushback, But Not Dismissal

Powell pushed back on the 1970s stagflation comparison, saying the Fed is managing the tension between its dual mandate goals, not responding to a full-blown stagflation environment. The distinction holds—for now. A Fed managing dual-mandate tension while oil trades at $109 and core PCE runs near 3% is not far from the definition it is trying to avoid.

On the Labor Market: Quiet Concern

The labor market message was more balanced than the statement suggested. Powell acknowledged real concern inside the Committee about very low job creation—noting that private-sector job growth is effectively near zero—while simultaneously saying the labor market is not a source of inflation pressure. The unemployment rate has changed little since last summer, and past rate cuts should help stabilize conditions.

The near-zero private-sector job growth figure is the one that deserves more attention than it received. If that continues, the employment leg of the dual mandate begins to deteriorate—and the path to cuts reopens regardless of where inflation is running.

On the SEP: Handle With Care

Powell downplayed the precision of the projections more than usual, saying this was “a time to take them with a grain of salt.” That is unusual candor about the limits of the Fed’s own models from a Chair at a post-meeting press conference. He nonetheless provided a clear read-through: the growth upgrade reflects stronger productivity, inflation forecasts moved up because of tariffs and energy, and while the median rate path did not change, there was a meaningful internal shift toward fewer cuts.

The Takeaway From the Presser

A Fed that still leans toward eventual easing—but only if inflation resumes improving. No urgency to cut. No appetite to rule out a more hawkish path if inflation stays sticky. The wait-and-see posture is genuine, not theatre. And the Middle East conflict is now formally embedded in the Fed’s reaction function—what happens in Hormuz before the next meeting will be a significant input to May’s decision.

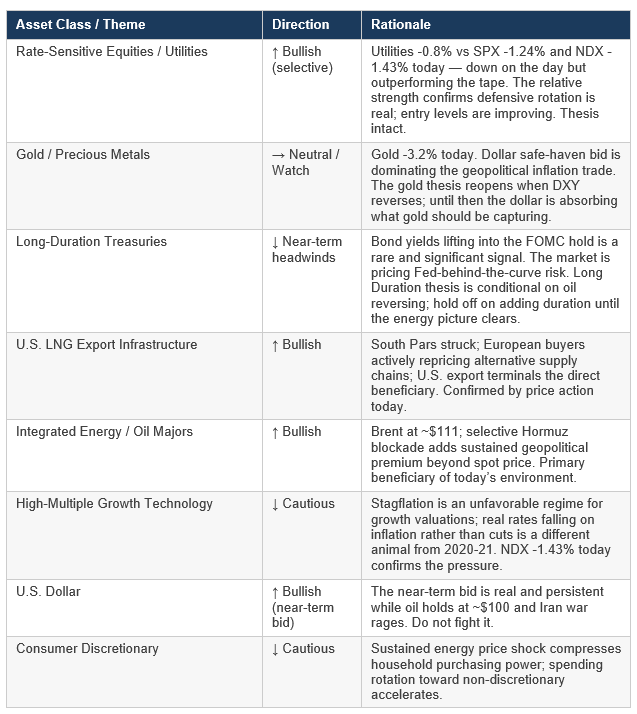

Positioning Implications

The initial knee-jerk read on unchanged dots—that bonds would rally and the dollar would soften—has not played out. By mid-afternoon, bond yields are lifting, DXY is firmer, and GLD is down over 3%. The market is delivering a harder stagflation verdict than the statement alone suggested: oil driving inflation higher, bonds selling off alongside equities, dollar holding its safe-haven bid. That is not the “unchanged dots = dovish” trade. It is the “the Fed is behind the curve” trade, and it changes the near-term positioning picture in three specific ways.

A Note on Utilities — Down But Outperforming

Utilities was down 0.8% today. That number deserves context: SPX is down 1.24% and NDX is down 1.43%. Utilities are not immune to a risk-off day with rising yields, but they are absorbing it considerably better than the broader tape. That differential — roughly 65 basis points of outperformance versus SPX and over 60 versus NDX in a single session — is the defensive rotation thesis expressing itself in real price action.

For longer-horizon investors, today’s weakness is not a thesis breaker. It is an entry point. The AI and data center structural demand story is unchanged. The rate path is unchanged. And the geopolitical environment is actively driving the kind of risk-off sentiment that historically pushes capital toward regulated, cash-flow-stable businesses. The sector is on sale relative to where it should trade in this macro environment.

A Note on Gold — Still Waiting

Gold has now failed to catch a safe-haven bid across an entire week of genuine geopolitical crisis. It is down over 3% today alone, and the week’s performance is net negative despite oil surging, a Hormuz blockade, regional energy infrastructure under attack, and an FOMC that confirmed higher inflation. The explanation is consistent throughout: the dollar is absorbing every flight-to-quality dollar, leaving gold starved of its traditional bid.

The gold thesis is not dead. It is conditional. It reopens when one of two things happens: the dollar safe-haven bid fades as geopolitical risk is priced in more fully, or the Fed signals a genuine pivot back toward cuts. Neither has happened yet. Until then, gold is not the trade—the dollar is.

A Note on U.S. LNG

The LNG angle deserves specific attention. South Pars, the world’s largest gas field, has been struck. European buyers who can no longer reliably source Gulf LNG are already repricing the value of alternative supply routes. U.S. LNG export infrastructure is the direct beneficiary. This is not a 48-hour trade.

The Bottom Line

Today’s FOMC—statement and press conference taken together—was a study in institutional honesty constrained by institutional limitations.

The statement told us: growth is okay, inflation is worse than we thought, the Middle East is the wildcard, and we are going to do nothing about any of it.

The press conference added the texture the statement omitted: core PCE is running near 3%, private-sector job growth is near zero, the tariff pass-through timeline is genuinely unknown, and five years of above-target inflation have eroded the Fed’s ability to credibly invoke the supply shock framework. Powell is more hawkish on inflation than the unchanged dots suggest—and more worried about the labor market than he is letting on.

And then the market delivered its own verdict. Bond yields lifted. The dollar held its bid. Gold fell 3%. The initial read that unchanged dots would soften the dollar and bid bonds did not play out. The market is not pricing this as a dovish hold. It is pricing it as a Fed that may already be behind the curve on a genuine stagflation shock. That is a harder verdict than the statement language alone implies—and probably the more honest one.

That is not indecision. It is a deliberate choice to hold the line while the fog of war—geopolitical and economic—remains too thick for confident policy action. Whether that choice proves correct depends on whether the Hormuz situation resolves in weeks or becomes a months-long structural shift in the global energy order.

Miran’s dissent record tells you the internal bias leans toward cutting when the window reopens. The inflation revision—and Powell’s frank acknowledgment that core PCE is near 3%—tells you that window may be narrower than the dots suggest.

Between a Fed that wants to ease and an inflation picture that won’t cooperate, set against a geopolitical backdrop that monetary policy cannot address—that is the question that will define positioning for the next quarter.

____________________________________________________________________________

The Macro Fireside is published by a trading veteran who has shepherded capital across decades and cycles in global markets through multiple asset classes. This note represents the author’s personal analysis and does not constitute investment advice. Past performance is not indicative of future results.

For professional enquiries please contact gs@macrofireside.com

macrofireside.com | © 2026 The Macro Fireside. All rights reserved.