The Realpolitik of selecting the Fed Chair

President Trump is to announce his choice for the Fed Chair soon, potentially as early as this upcoming week. The FOMC meets January 27-28 to decide monetary policy, and the timing of any announcement in proximity to that meeting would be notable given the unprecedented public debate surrounding what is typically a routine presidential decision. The President has openly accused the Fed chair of lacking competence for not lowering interest rates in time (Jay “too late” Powell in his recent Davos speech). The DoJ’s criminal investigation into Powell regarding his Senate testimony on Fed building renovations brought things to a boil, and Powell for the first time openly called it a pretext, stating the action was a consequence of the FOMC not doing the President’s bidding on interest rates. Such acrimony has rarely been seen at the nation’s highest policymaking levels — fiscal and monetary.

Now the time comes to choose Powell’s successor and reportedly there are four men in the running — Fed Governor Chris Waller, former Fed Governor Kevin Warsh, current Chief Economic Advisor Kevin Hassett, and BlackRock’s Rick Rieder.

To be clear, the choice of Fed chief is less about competence and track record — which all these candidates possess — than about what works for the White House across several dimensions, including critically the ability to secure Senate confirmation in an environment where the DoJ investigation has heightened scrutiny around institutional autonomy.

Governor Waller currently serves on the FOMC, has taken measured stances on monetary policy, and is a known commodity to markets who can coalesce a divided Fed. His technocratic profile and consistent advocacy for rate cuts without appearing politically captured makes him attractive. At a recent Yale event, 81% of CEOs polled chose Waller as their preferred candidate. His main limitation may be a lack of the personal closeness to the president that Trump typically values in top appointments.

Kevin Warsh presents a more complex calculus than his hawkish reputation might suggest. While he was distinctly hawkish during his previous Fed tenure, advocating that “inflation is a choice” and warning about debt’s influence on Fed decision-making, his candidacy has gained renewed traction because of the DoJ investigation. Senator Thom Tillis’s pledge to oppose any Fed nominee until the investigation is resolved has elevated the importance of credible institutional distance. Warsh is widely viewed by markets as the “independence candidate” — institutionally orthodox and skeptical of political pressure. In an environment where Senate confirmation has become uncertain rather than merely ceremonial, Warsh’s credentials as someone who can credibly defend Fed autonomy may outweigh concerns about his historical hawkishness, especially if he signals flexibility on the path to neutral rates.

Kevin Hassett was the front-runner until Trump’s recent comment about wanting him to continue in his current position, presumably to avoid the optics of a White House-Fed nexus running policy. This could be genuine — Hassett’s close relationship with Trump raises legitimate concerns about whether markets would view him as institutionally credible or a political extension of the administration. Yet with Trump, such statements are not always definitive. Hassett remains a known dove and trusted lieutenant, and the president’s tendency for surprise moves means his chances of getting the Fed job, while diminished, are not exactly zero. The question is whether Trump values loyalty and policy alignment enough to weather the confirmation battle and market skepticism that a Hassett nomination would invite.

In the same breath, I should note that Trump has lamented that Treasury Secretary Bessent wants to remain at Treasury but would be his ideal choice for the job. While Bessent would be an agreeable choice to markets as a practitioner and close confidante who would receive relatively smooth Senate confirmation, his preference to stay at Treasury appears genuine.

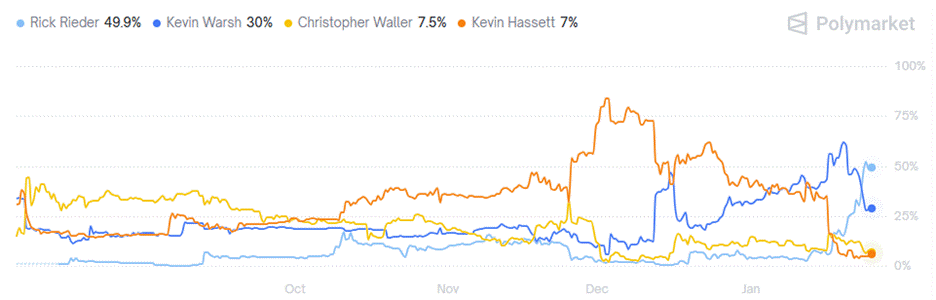

That brings us to Rick Rieder, whose candidacy has surged dramatically in recent days. Following Trump’s description of him as “very impressive” at Davos, prediction markets have moved sharply in Rieder’s favor — he now commands 45-48% odds versus Warsh’s 30%, a remarkable late-stage momentum shift. As BlackRock’s Chief Investment Officer for Global Fixed Income overseeing $2.4 trillion, Rieder brings Wall Street credibility and has been vocal about taking policy rates down toward 3%. His relationship with BlackRock CEO Larry Fink — whose rapport with Trump improved notably at Davos — adds another dimension.

Rieder may offer Trump several advantages simultaneously. He has never worked at the Fed, making him appear less institutionally entrenched — attractive both to Trump (who values outsiders) and to senators wary of business-as-usual after the DoJ investigation. Bloomberg reports he’s shown willingness to reform the central bank, yet his market practitioner background and the positive response from bond market participants when his name surfaces suggest he wouldn’t be viewed as a destabilizing choice. Some White House sources believe Rieder could be easier to confirm than Hassett because he lacks the appearance of political capture, while still being aligned with the administration’s preference for lower rates.

The obvious question: can someone with no Fed or policymaking experience successfully navigate a potentially divided FOMC while learning on the job? This is a legitimate concern, but in the current political economy, it may matter less than whether the nominee can survive Senate confirmation and maintain market confidence while pursuing the administration’s rate preferences.

So, what’s my read? Rieder has the momentum and may offer Trump the best of both worlds — alignment on lower rates without the political baggage that would make Hassett’s confirmation a battle. If Rieder’s interview went as well as reported and he can credibly maintain the Fed’s institutional distance while delivering cuts, he gets the nod. Hassett remains the fallback if Trump decides he values loyalty over confirmability, or if Rieder’s lack of policymaking experience becomes disqualifying in Senate deliberations.

Waller and Warsh? Both viable, but they solve different problems than the one Trump seems most focused on — getting rates down quickly without a protracted confirmation fight. Waller is the safe choice if Trump wants minimal friction. Warsh is the credibility play if the DoJ investigation blowback gets worse. But right now, the smart money is moving toward Rieder.

With markets currently pricing the first rate cut around mid-year, the job of the new Fed Chair, who will assume office in May when Powell’s term ends, should be straightforward initially — bring forward a rate cut to spring or early summer. All the candidates can deliver that. What happens beyond that first cut is foreseeable. The fundamental tension between institutional autonomy and political pressure will persist. The new chair will need to balance the administration’s clear preference for significantly lower rates against the Fed’s dual mandate and the judgment of a diverse FOMC.

Pragmatism and power dynamics will come to the fore, hopefully guided by the scruples of monetary policymaking. That is Realpolitik at work!

My commentary of January 14, 2026, which is a prequel to this piece follows:

The "Independence Premium" and the 2026 Rate Path

(Originally published on LinkedIn, January 14, 2026)